(January 21, 2026): The past year has been rough for many dental practices around the country. After declining during COVID, government and private payor audits of dental claims rose sharply in 2024 and continued to increase in 2025. The question we are now being asked by our dental clients is whether these activities will continue in 2026. In this article, we examine several factors that we believe will affect both government and private payor enforcement. We also review the dental business practices and alleged improper conduct that is likely to place your practice under the scrutiny of law enforcement and Special Investigative Units (SIUs) working for private dental payors. We also lay out recommendations for responding to dental claim audits.

I. Entities Likely to Initiate Dental Claim Audits in 2026:

The following federal and state law enforcement, government contracted audit entities, and private payor Special Investigation Units (SIUs) are actively conducting Medicare, Medicaid, TRICARE, and private payor dental claim audits.

- MFCU Auditors: Medicaid Fraud Control Units (MFCUs) are the primary state law enforcement entities likely to audit your Medicaid dental claims. MFCU audits can result in administrative sanctions, civil penalties, and criminal prosecution. The primary dental claim risk issues currently the focus of MFCUs around the country include, but are not limited to:

- Clinics that perform high volumes of pediatric pulpotomies and stainless-steel crowns.

- Clinics that perform high volumes of procedures that require the use of physical restraints, such as papoose boards.

- Clinics that have billed for extractions or root canals for patients who have already undergone these procedures.

- Clinics that perform high volumes of surgical extractions vs. simple extractions.

- Allegations that a clinic has been paying community “recruiters” to steer Medicaid beneficiaries to their practice for dental care and treatment.

- MAC Contractors: Medicare Administrative Contractors (MACs) are primarily involved in the processing of Medicare fee-for-service Part A and Part B claims within specific geographic jurisdictions. Their dental claim audits are limited to the narrow group of claims that qualify for coverage and payment by Medicare.

- TRICARE Auditors: TRICARE auditors and their support contractors audit a wide variety of medical and dental claims submitted in connection with active-duty service members and their families, eligible military retirees, and their families, and select groups of other eligible individuals. United Concordia has been contracted by TRICARE to audit a full range of routine dental procedures billed to the payor.

- UPIC Contractors: While Uniform Program Integrity Contractors (UPICs) are best known for their audits of Medicare Part B fee-for-service claims, in recent years, they have increasingly targeted dental practices due to significant identified program integrity risks in Medicaid dental programs. UPICs have also expanded their audits of Medicare Advantage and Medicaid Managed Care claims. Notably, UPICs were permitted to audit Medicaid claims since their inception in 2016. Nevertheless, they did not fully move into the Medicaid space until 2022, after the issuance of a report by the Department of Health and Human Services (HHS), Office of Inspector General (OIG), recommending that they conduct more Medicaid audits. Specific dental risk issues audited by UPICs have included Medicaid pediatric dental services (such as stainless-steel crowns).

- RAC Auditors: The Affordable Care Act (ACA) expanded the Recovery Audit Contractor (RAC) program to Medicaid and required the states and the District of Columbia to establish programs and contract with one or more Medicaid RACs to audit Medicaid claims and to identify underpayments and overpayments.

- CERT Contractors: Comprehensive Error Rate Testing (CERT) auditors focus on Medicare fee-for-service Part A, Part B, and DMEPOS claims, including Medicare dental claims.

- SMRC Contractors: Supplemental Medical Review Contractor (SMRC) auditors have been contractors by CMS to conduct nationwide audits of Medicare Part A, Part B, Medicaid, and DMEPOS claims. While the scope of dental-related claims audited by SMRC auditors has been limited, one area that has been reviewed is HCPCS G0330 claims for dental rehabilitation under anesthesia. SMRC auditors have also looked at dental services that are so integral to other medically necessary services that the clinical success of the service is dependent upon or “inextricably linked” [1] to the dental services. While G0330 is a facility code, the actual dental procedures performed by the dentist are reported using CDT codes. Over the last two years, CMS has added a substantial number of dental procedures to the “Covered Procedures List” that may be performed in Ambulatory Surgical Centers (ASCs). Examples of dental procedures that may be covered if they are inextricably linked to a covered medical condition include:

- Tooth extractions to eliminate infection.

- Diagnostic exams and radiographs.

- Medically necessary dental rehabilitation for high-risk patients who require general anesthesia.

- Private Payor SIUs: All commercial dental insurance payors have established in-house Special Investigative Units (SIUs) to audit dental claims submitted in connection with the care and treatment of their enrolled beneficiaries.[2]

II. Dental Risk Areas Likely to be Targeted by Government Auditors and Private Payor SIUs in 2026:

In recent years, both federal and state prosecutors have aggressively increased their investigation of alleged improper conduct and/or fraudulent billing practices by dentists and their practices. In our defense of dentists and their practices, federal and state regulators, and private payor SIUs regularly raise the following allegations when pursuing cases against our clients.

- “Upcoding.” Upcoding occurs when a dentist bills a payor or patient for a more severe dental procedure, or at a higher level of service, than was rendered. Improper upcoding is one of the primary reasons payers cite when denying claims during audits. Auditors will look at the frequency and scope of upcoding when assessing whether upcoding was a mistake OR may be indicative of a pattern or practice of intentional misrepresentation or fraud.

Example:

Actual dental service provided -- Routine adult dental cleaning (prophylaxis). CDT Code D1110.

Dental service billed to payor -- Deep cleaning (scaling and root planing). CDT Code D4341. - Billing for dental services that were never provided. Both government and private payors like to characterize this as dental insurance fraud. After representing numerous dental providers accused of this type of billing fraud, we have found that, in many cases, the services at issue were, in fact, performed. Unfortunately, the dental provider has failed to properly document the service or procedure in the patient’s dental record. This is especially prevalent when billing for radiographs. We have seen multiple cases where the practice cannot locate digital images of the radiographs, even though it uses a digital system that is supposed to maintain image backups.

While a dentist may be able to explain discrepancies, we have seen cases where mistakes were made and the billed dental service was, in fact, not provided. For example, if a dentist bills a payor for a Dental Filling, Amalgam (One Surface, Posterior/Primary), CDT D2140, it will be relatively easy for a payor to confirm that the procedure was (or was not) performed by reviewing the patient’s radiographs taken on the date of service and on subsequent visits. - Utilizing improper billing and/or coding practices when submitting dental claims. Improper billing and coding of dental services and procedures can take many forms. For example, in the case below, the defendant dentist was supposed to be paid based on each patient visit, not based on the dental services rendered.

• California. In this case, the California Attorney General’s Office charged a California dentist and five employees of his practice with “Conspiracy to Commit a Crime” and Medi-Cal Fraud. Both charges are felonies. At the time of the fraud, the defendant dentist’s clinic contracted with a local Federally Qualified Health Center (FCHQ) that provided a wide variety of medical and dental services to Medi-Cal beneficiaries. The government alleged that the defendant dentist was supposed to be reimbursed for each patient visit, NOT for the specific dental services performed on the Medi-Cal beneficiaries. The government further alleged that some dental services billed were either not rendered or were not performed over multiple days, as claimed by the defendants. The government has alleged that the defendant dentist and his employees fraudulently billed more than $847,000. As of December 2025, the criminal case against the dentist and his employees is ongoing and has not reached a final resolution or sentencing.

- Misrepresentation of their licensure status or other credentials. Unfortunately, state regulators have identified multiple instances of this. Improper conduct of this type can take various forms. The most common is practicing dentistry without a license. Another form of misrepresentation occurs when an individual is licensed to practice dentistry but has been excluded from participation in Federal health care programs due to a qualifying conviction or another basis for exclusion. A third variation occurs when non-credentialed dental services are billed under a credentialed dentist's number. Finally, we have examined situations where a licensed dentist is on probation for substance abuse and is required to practice only under supervision and/or may be prohibited from administering certain medications for pain. Examples of these variations are discussed below.

Example #1: Practicing dentistry without a license.

- Georgia. In this recent case, an individual operated a cosmetic dental practice in Atlanta and marketed himself as “Atlanta’s Top Veneer Specialist.” He performed dental procedures (veneers) and charged patients thousands of dollars for his work. Law enforcement alleges that the individual had never held a dental license. In November 2025, he was indicted on multiple counts of practicing dentistry without a license, conspiracy to commit insurance fraud, and is currently facing a litany of other charges. The defendant is scheduled to be arraigned in January 2026.

- Massachusetts. In this case, the unlicensed manager of a dental practice was alleged to have performed and billed MassHealth (Medicaid) for dental services, even though the services billed must be performed by a licensed dentist. State prosecutors have indicted the unlicensed manager, alleging that he committed Medicaid fraud, unlicensed practice of dentistry, and assault and battery (stemming from alleged harm caused by his unlicensed extraction of a patient’s tooth). The defendant has pleaded “Not Guilty.” This case is still pending.

- Florida. In this case, two individuals operated a dental practice out of a bus. They allegedly provided dental services to multiple patients and used prescription drugs in their treatment of the patients. After conducting an undercover investigation of the duo, they were arrested and charged with practicing dentistry without a license.

- Maryland. In 2015, the Maryland Board of Dentistry revoked the license to practice dentistry of one of its dentists. The government subsequently alleged that from 2015-2023, the unlicensed dentist continued to practice without a license. As a result of the investigation, the defendant pleaded guilty to one count of defrauding a state health plan, the Medicaid program, and one count of practicing dentistry without a license. More specifically, the government alleged that the defendant used the names, provider numbers, and professional credentials of four other licensed dentists to improperly submit claims under the Medicaid program. Last year, the defendant was initially sentenced to 18 months of home detention, with his remaining 3.5 years suspended, and 5 years’ probation. Later in the year, the government alleged that the defendant violated the terms of his probation. He was then sentenced to 18 months in jail.

Example #2: Billing for dental services performed by an individual who is excluded from participation in federal health care programs.

- Maryland. In this case, the owner of a dental practice (a licensed, practicing dentist) employed an individual who was excluded from participation in federal health benefit programs. The excluded dentist provided dental services to patients that were billed to a federal health care program. Upon investigation, the owner of the dental practice agreed to pay civil monetary penalties to resolve his wrongful submissions of claims for dental services performed by an excluded individual.

Example #3: Billing for dental services performed by a non-credentialed dentist under the billing number of a credentialed dentist.

- Indiana. In this case, the government alleged that an Indiana dental practice submitted claims to the state Medicaid program for dental services performed by non-credentialed dentists, using the names of credentialed Indiana Medicaid dentists. The practice was assessed more than $125,000 in civil monetary penalties by HHS-OIG.

- Massachusetts. Notably, this case involved a Massachusetts dental school. The OIG alleged that the dental school submitted claims to Medicare[3] for dental services that were provided by non-credentialed dentists. The OIG further claimed that in some cases, the patients’ dental records did not support the level of dental services billed. The dental school was assessed more than $840,000 in civil monetary penalties.

Example #4: Improperly allowing the purchaser of a dental practice to utilize the seller’s NPI while credentialing for the buyer takes place. We get it – depending on the payor, successfully working through the credentialing process can take several months. We recently discussed the “credentialing problem” with a lawyer colleague, Jordan Uditsky.[4] He has repeatedly seen situations where the individual or entity purchasing a dental practice has sought to include a specific provision in the purchase agreement titled “Temporary Use of a Seller’s NPI and Payor Contractors,” or something similar. Just to be clear – this is not permitted. You cannot use another provider’s NPI while you are working through the credentialing process. Nor can you temporarily permit another dentist to use your NPI for billing purposes. If you engage in this type of conduct and submit dental claims to Medicaid or another federal health care benefits program where the identity of the rendering dentist is falsified, you may be prosecuted for fraud. Similarly, if the payor is private, at a minimum, this would be a violation of your contractual obligations. Additionally, depending on the facts, the private payor’s SIU may decide to make a referral to law enforcement. Federal prosecutors could allege that such conduct constitutes a violation of 18 U.S.C. 1347.[5]

Example #5: Billing for dental services performed by a licensed dentist whose license is restricted. Licensed healthcare professionals can face significant restrictions on their ability to practice due to state disciplinary actions, hospital privileging issues, restricted licenses due to a history of substance abuse, and other barriers—even when their licenses remain valid. These mechanisms protect patients and the integrity of the healthcare system, but they also show that licensure alone does not guarantee the right to practice in all settings or circumstances. When a dentist violates the restrictions placed on their license, the State Dental Board typically sanctions them.

- Providing dental services outside their scope of practice. Dental practices have faced significant legal and regulatory consequences for billing insurers or Medicaid for services performed by individuals outside their authorized license scope.

- Georgia. In this case, a Georgia dental practice was alleged to have permitted dental assistants and hygienists who were not authorized under Georgia law to perform x-rays and other services that cannot be performed without direct supervision by a Georgia licensed dentist. These actions alleged violated both Georgia state law and Medicaid’s billing rules. To resolve these allegations, the defendant dental practice agreed to pay $3 million to the government.

- National dental chain. In this case, a national dental chain and its management company were alleged to have permitted unqualified personnel, such as dental assistants, to perform pulpotomies and other dental procedures that were outside of their legal scope of dental practice. The government sued the defendants under the False Claims Act. The defendants agreed to pay more than $23 million to resolve the False Claims Act allegations levied against them.

- Offering kickbacks to referral sources or patients to steer business to your dental practice.

- Connecticut. Last month, two Connecticut dental providers were alleged to have violated both the Federal False Claims Act and Connecticut’s state False Claims Act. These alleged violations arose out of a larger investigation by federal and state law enforcement agencies into fraudulent activity by health care providers that submitted kickback tainted claims to Connecticut’s Medical Assistance Program for services to Medicaid patients referred to the providers by third-party “patient recruiting” companies. In this case, the two dentists and their practices were alleged to have paid a patient recruiter for each Medicaid patient referred to their dental practices for care. The improper referral and payment to the recruiter violated both the practices participation agreement with Medicaid and constituted a violation of the criminal Anti-Kickback Statute.[6] To resolve the False Claims Act violations asserted. The two dentists agreed to pay more than $700,000 to reimburse Medicaid for the improper claims submitted.

- Connecticut. In this Medicaid fraud case brought by the U.S. Attorney’s Office for the District of Connecticut, the defendant dentist pleaded guilty to conspiring with several other individuals to pay kickbacks to patient recruiters who enlisted individuals covered under Connecticut’s Medicaid program to attend dental appointments and receive dental services by the defendant dentist. These dental services were then wrongfully billed to Medicaid. The recruiters allegedly paid a portion of the kickbacks they received to the Medicaid patients to serve as an incentive to attend the scheduled dental appointments. Between 2016 and 2023, the government estimated that the defendant dentist received approximately $2.2 million in reimbursement from Connecticut Medicaid for the dental services rendered to patients recruited in connection with this kickback scheme. As part of her plea, the defendant dentist forfeited $500,000 and was sentenced to two years of probation.

- Texas. In this case, the dentist who owned a Houston dental practice was ordered to serve 120 months in Federal prison and pay restitution totaling more than $4 million for his role in a pediatric Medicaid fraud scheme. In this case, Federal prosecutors alleged that the defendant billed Texas Medicaid for dental services that were not rendered OR were performed by unlicensed individuals. The government also alleged that the defendant paid kickbacks to marketers and caregivers of Medicaid insured children in exchange for referring the patients to the practice.

- Failure to return overpayments and/or unclaimed patient balances. There is a basic rule at play here – “If it isn’t yours, give it back.” Unfortunately, not all health care providers have adopted this policy. There are two primary ways that this risk issue may arise: (1) Overpayments, and (2) Patient credit balances. Both compliance risks are discussed below.

- Overpayments to the government. In recent years, both federal and state regulators have aggressively pursued damages against health care providers, including dentists, who fail to report and return overpayments to Medicare and Medicaid. Under the Affordable Care Act (ACA),[7] providers have an affirmative obligation to report and return overpayments to the government promptly. Was the “error” or other action that resulted in an overpayment an isolated event? If not, you will need to review prior claims and repay all overpayments to the payor. Keep in mind – your obligation to repay funds that do not belong to you extends far beyond the provisions of the ACA. Among its provisions, the ACA made clear that the knowing retention of an identified overpayment violates the False Claims Act. Once you have returned any overpayments to the government, any associated co-payments paid by beneficiaries must also be returned.[8]

- Overpayments owed to a private payor. Dental practices are obligated by law and by their contractual obligations to return any overpayments or incorrect collections owed to a private payor. Importantly, even if a private payor returns your check, any associated overpayment still does not belong to you.

- Credit balances. Do you have credit balances and/or unclaimed patient funds on your books? Credit balances never belong to you. All states have passed escheat laws which cover overpayments and credit balances.

- Improperly using medications in “single dose” vials in treating more than one patient. Using remainders from "single-dose" or "single-use" vials for different patients is illegal primarily due to the severe risk of life-threatening infections and strict federal regulatory standards.[9] Common dental medications available in single-use vials include local anesthetics, sedatives, and emergency drugs. These vials are intended for a single patient but often contain more medication than needed for a single procedure, resulting in leftover doses. Regulatory guidelines prohibit using these remainders for other patients. Moreover, billing multiple times for a single vial is both a safety violation and constitutes billing abuse.

- Routine failure to collect dental copayments and deductibles. While often motivated by good intentions, providing patients with free or discounted items or services—such as gifts, incentives, waiving copays, complimentary screenings, or free medical supplies—can potentially breach both federal and state regulations regarding improper inducements, particularly when the patient receives benefits from federal healthcare programs.Understandably, authorities are concerned that improper incentives to patients (such as the routine waiver of copayments) can lead to unnecessary use of services, influence clinical decision-making, and drive-up costs for programs like Medicare and Medicaid. Violations related to unlawful inducements may result in administrative, civil, or criminal consequences, mandatory repayment to government health programs, and even exclusion from participation in those programs. Additionally, private insurers are increasingly scrutinizing and opposing these practices. Healthcare providers and their teams must be well-versed in relevant laws and restrictions to avoid these risks.Interestingly, law enforcement and State Dental Boards are not the only entities concerned about the improper waiver of copayments. In the case below, a state dental association sought injunctive relief against a New Jersey dentist alleged to be routinely waiving patient copayments.

- New Jersey. In this 1983 case, the New Jersey Dental Association, NOT the New Jersey State Board of Dentistry, sought an injunction against a New Jersey dentist who was alleged to have waived copayments for 97 percent of his patients. Moreover, the defendant dentist was alleged to have advertised that he would waive copayments. The New Jersey Dental Association claimed that the dentist’s activities were fraudulent and constituted unfair competition. A Superior Court of New Jersey agreed and ordered the defendant dentist to either bill insurers for the amounts he collected or inform payors of any waivers provided to patients.

- Improper unbundling of dental services. “Unbundling” refers to the illegal dental billing practice of taking a multi-part dental service that is typically billed under a single code and breaking it up into its component parts which are then separately billed to a payor. Dental providers have been known to engage in this improper billing practice when the reimbursement sum of the component parts is greater than the reimbursement if the dental service is billed under the consolidated code. An example of unbundling would include performing a simple, erupted tooth extraction that is normally billed as a CDT D7140 and breaking it down into its component parts and billing separately for local anesthesia, incisions, drainage, and sutures.

- Misrepresenting dates of service. Misrepresenting the date of a dental service to ensure insurance coverage is considered insurance fraud and is both unethical and illegal. This practice involves submitting a claim with an incorrect date of service—such as changing the date to fall within a patient’s coverage period or after a waiting period has ended—so that the insurance company will pay for the procedure when it otherwise would not qualify for payment.

III. Impact of Private Equity’s Expansion into Dentistry:

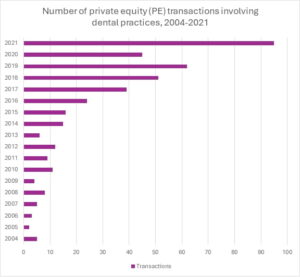

From 2004 through 2021, private equity (PE) firm purchases of dental practices steadily increased.[10] From 2022 through 2024, PE activity declined due to COVID-19. According to the nonprofit watchdog “Private Equity Stakeholder Project,” post-COVID, the acquisition of dental care practices has been frenzied. In fact, the roll-up of dental care providers in 2024 was the highest deal activity of any health care category.[11] Although the final 2025 numbers are still being compiled, this past year has been similarly busy. Dental practices remain a primary target for PE. As the baby boomer generation ages into eligibility for Medicare Advantage,[12] Original Medicare, and Medicaid Managed Care plans, the scope of dental services covered under Federal health care benefits plans will undoubtedly increase. As dental coverage expands, both government and private payor dental plans have established more stringent screening protocols and implemented intensive auditing programs to help eliminate fraud and abuse. Moreover, a number of State Attorneys General have weighed in and expressed a variety of concerns over the entry of PE into the healthcare marketplace.[13] Initially, PE firms focused their acquisition efforts on general dentistry practices. More recently, PE firms have been targeting high-margin dental specialties, such as oral surgery, endodontic, and pediatric dental practices.

In recent years, State Attorneys General have responded to the expansion of private equity into health care by increasing law enforcement scrutiny, supporting the passage of new legislation, imposing mandatory transaction reviews, and expanding their examination of corporate practice of medicine (CPOM) issues. They have also called for greater Federal oversight. At least seven states enacted laws in 2025 to increase oversight.[14]

Both federal and state prosecutors have actively audited and investigated PE firm owned health care companies. In doing so, they have identified a variety of cases where the company engaged in alleged improper conduct. Setting aside the considerable antitrust concerns that have been expressed by the DOJ and the Federal Trade Commission (FTC), there have been a variety of common health care fraud enforcement actions taken against PE owned health care companies. Examples are set out below.

- Aggressive billing and unnecessary services. There have been ongoing concerns that, due to their business focus, PE Firms pressure providers to perform more dental procedures and bill payors more aggressively, sometimes resulting in improper upcoding, the provision of medically unnecessary dental services, and the billing of dental services that are not documented in patients’ dental records. While specific examples involving dental services are sparse, there have been “upcoding” cases involving other health care services owned in whole or in part by PE firms.

- Utilizing unlicensed and/or unqualified staff to perform dental services. Many of the services performed by health care providers require licensure and/or specific training for the services to be rendered to patients. Using unlicensed or unqualified staff to perform these services is improper and is outside the scope of their authority. Similarly, even if a staff member performing a service is properly licensed, if the individual has not been properly credentialed by the beneficiary’s insurance company, the uncredentialed provider’s services may not qualify for coverage. Depending on the facts, the services of an uncredentialed provider may qualify to be billed under the NPI of a supervising physician or dentist. This type of billing scenario is referred to as “Incident To” billing. Unfortunately, very few state Medicaid dental payor plans permit incident to billing.[15] Similarly, most private dental payors do not permit incident to billing. As a final point, please note that even if a particular Medicare Advantage, state Medicaid, state Medicaid Managed Care, or a private payor dental plan permits incident to billing, there are multiple requirements that must be met in order for the service to meet all of the incident to requirements for coverage, coding and billing.

- Staffing cuts and utilizing unqualified staff. There have been instances in nursing homes where the PE-owned facility was alleged to have reduced the number of nurses and physicians to cut costs. In some instances, facilities were alleged to have hired less costly, often unlicensed, or unqualified to fill the roles left by cutting more expensive nurses, etc. Once again, dental practices can run into trouble by taking similar actions to reduce expenses. For example, although not all states require dental assistants to be fully "licensed," all states have implemented regulations to restrict the kinds of services and procedures that they may perform. Some states, such as New York and California, have imposed specific licensing requirements on dental assistants. We have defended several cases where a government or SIU audit found that the services performed by a dental assistant were outside the scope of services permitted by the state.

- Asset Stripping & Financial Instability. Government regulators have expressed unease that once PE firms acquire health care companies, overly aggressive actions to reduce expenses and siphon off assets can result in the health care company becoming insolvent. This is especially problematic in health care companies with a large Medicaid payor base and in those companies that serve rural communities. Unfortunately, both of these factors are common when dealing with dental practices.

- Conflicts of interest for dental providers. While profitability is undoubtedly important, government regulators have voiced their concerns that the ever-present drive for profits (by cutting expenses and/or focusing on billing for more dental services at a higher price point) can place dentists and other licensed health care professionals in an untenable position of placing profits ahead of quality patient care. This can lead to bad decision-making by dentists and could harm patients.

Why does this seem to regularly occur? On a fundamental level, PE firms often fail to adequately assess compliance risks in healthcare due diligence because they prioritize financial metrics, lack specialized healthcare expertise, underestimate regulatory complexity, and are incentivized by short-term returns. Their due diligence teams are often staffed by generalists with only limited experience, if any, representing health care providers and suppliers in regulatory and reimbursement matters. Business practices that may be perfectly legal in other industries are often illegal in health care. This leads to repeated oversights and exposes them to significant legal and financial liabilities.

IV. Steps to Take Now, BEFORE Dental Claim Audits are Initiated:

- Understand the rules of the road: It is never too early to think about your obligations as a dental provider to ensure that the dental services you perform meet a payor’s coverage, documentation, coding, and billing requirements. Before enrolling as participating provider in a dental plan, you should carefully review the proposed payor contract. This can be an overwhelming process, and many dentists delegate these enrollment tasks to their office managers or billing staff. Be careful. There may be a tendency for your administrative staff to focus on reimbursement rates and one or more of the other important terms of the participation agreement can be missed. We strongly recommend that you, not just your administrative staff, read the contract and familiarize yourself with the terms of the agreement. Points to consider include, but are not limited to the following:

- Keep a copy of your contract. While this sounds easy, it often is not. These days, payors maintain their provider contracts online. Print out a copy of the contract you execute when it is finalized. Payors are constantly tweaking their agreements and do not always note when changes to the contract or fee schedule have been made. You need to know the terms of your agreement, not what is currently being required by the payor.

- Fee schedules. Understand how your reimbursement rates are structured. Does your contract include a “most favored nations clause” where you agree not to charge the insurer a higher rate than you charge to any other payor? We have seen cases over the last year where a well-known private dental payor raised this issue in their audit of our client’s dental claims. It may be worth your time and money to engage a consultant to try and negotiate one or more payors’ fee schedules.

- Coverage and treatment limitations. Do not conflate “coverage” with “medical necessity.” Although you may believe that it was medically necessary to perform a dental procedure on a patient, a payor may or may not cover that procedure. Check your contract! Keep in mind that coverage requirements often differ from one payor to another. Additionally, you need to review both the number of treatments and frequency limitations that may be imposed under the terms of a contract.

- Documentation requirements. When documenting dental services, there are three sets of rules that you consider. First, what does your state require in terms of documentation? For example, Texas has enacted minimum regulatory guardrails that must be followed when documenting the dental services you provide.[16] Second, review your payor contract and any additional ancillary guidance that is referenced by the contract. Specific documentation requirements may be mandated by the payor. Should you fail to meet these documentation requirements, your claims will be denied. Finally, there are specialized dental procedures for which no documentation guidance may have been issued by your payor. Dental subspecialty associations may have issued guidance on how to best document these procedures. In the event of an audit, a payor may point to that guidance as the standard of care for documenting the provision of those services.

- Filing deadlines. How long do you have to file a claim? Filing deadlines vary from payor to payor. It is often difficult to show “good cause” for missing a filing deadline. Make sure you know when your claims must be filed.

- Reopening and recoupment deadlines. How far back can a payor audit and seek to recoup alleged overpayments? It is important that you know this information so that you can object if the payor tries to reopen claims that are outside of the period that may be reopened.

- Collection of patient copayments and deductibles. As previously discussed in this article, the routine waiver of copayments and deductibles may give rise to kickback concerns if the payor is a federal health benefit program. If a private payor is involved, such conduct could constitute a breach of your contractual obligations.

- Implement an effective Compliance Program. While compliance programs were initially voluntary but recommended, federal legislative changes[17] and state payor contract obligations now typically mandate the implementation of an effective compliance program. For example, in New York and Texas, all Medicaid providers are now required to have an effective compliance plan in place. Compliance is no longer voluntary, it is mandatory.

- Review your claims on an ongoing basis. An effective compliance plan typically includes seven core elements. The most important of these seven is “Internal Auditing and Monitoring.” Dental practices should compare their actual documentation, coding, and billing practices with the payor’s rules. Any “gaps” between the applicable requirements and a provider’s actual practices must immediately be remedied. Additionally, should these “gaps” represent an overpayment, a dental provider must promptly repay the overpayment to the appropriate payor. Prior to conducting a “gap” analysis, you should contact your legal counsel for advice and assistance.

Payor audits can be scary – no doubt about it. A third party will be reviewing your patients’ dental records, evaluating the treatment plans or plans of care that you have created. They will also review your radiographs to determine whether the dental procedures you performed are supported by the images you have maintained in the patient’s dental records. They will also be examining your billing practices. Have you consistently tried to collect co-payments and deductibles from patients? Have you charged the dental plan at the same rate as what you have charged uninsured patients? Look at your billing records, especially the ADA Dental Claim Form submitted to the payor for each date of service. Is each service or procedure properly documented in the patient’s dental record?

V. Responding to Dental Claims Audit in 2026:

Regardless of how diligent you work to ensure that your dental services are properly documented and billed, there is a high likelihood that your dental practice will be audited by one or more payors or law enforcement entities. When this occurs, you should consider the following:

| Actions to Take After Receiving a Request for Dental Records in an Audit |

|---|

| Upon receiving an audit letter, contact your attorney. The goal here is to make sure that your rights are protected and that you can properly respond to the payor’s request. Attorneys who regularly represent dental providers in audits can provide insights into the focus of the payor’s audit. Additionally, legal counsel may be able to get the scope of a payor’s review narrowed and may be able to secure additional time for you to submit the information requested. |

| Assess the auditor’s timeliness of review. Dental providers should carefully assess the claims at issue to determine whether they have been evaluated in a timely fashion. What does your provider agreement say about how long a payor has to reopen a claim? |

| Review past dental claims audits and evaluations. Has this payor reviewed your dental claims in the past? If so, what was the focus of their prior reviews? Were prior problems addressed and remedial steps taken? |

| Assemble the dental records requested. Take the time to assess the specific claims at issue and the supporting documentation in each file. Are there additional places (e.g., files in storage, lab results, radiograph images on the server) where additional supporting documentation may be kept? If the documentation is incomplete, can it be further supported with records of purchase orders (drugs, dental supplies)? Are there any referring or ancillary providers that might have additional supporting documentation (e.g., referrals or orders from another dentist, laboratory test results, or radiograph images)? |

| Either submit your dental records within the period requested or get an extension. The best way of avoiding overpayment is to ensure that a reviewer has all the relevant documentation that supports the coverage and payment of the claims at issue. Ensure that dental records and supporting documentation are forwarded within the time required. Payors will not hesitate to deny claims and assess an overpayment if the supporting dental records are not received in a timely fashion. |

| Send in supplemental information immediately. Should you identify additional supplemental information which supports the dental claims at issue, submit this additional documentation immediately before the payor issues the results of its review. |

| Are there indications that the payor intends to extrapolate damages? Carefully review all correspondence from the payor related to the audit. If the records request describes the group of dental claims selected for review as a “statistically relevant sample” or uses similar descriptive terminology, this may be an indication that the payor intends to extrapolate damages. Check your contract! Is that permitted? |

| Are your dental records legible? Although most dental providers now use an electronic dental records system, practices still heavily rely on written dental records. Are they legible? Handwritten portions of a dental record must be legible by an average reviewer, not merely by the passage’s author. Discuss this issue with your attorney. You may need to submit the original handwritten records along with a transcribed copy of the record to the payor. |

| Supplementing a record and / or correcting illegible or erroneous words, phrases, or passages. If a supplement to a record, a change or a correction to a word or passage is necessary, you should not erase, white-out, scratch out or use a marker to conceal the original remark. First, you should never backdate a document. If you find that an affidavit or supplement to a record is needed, it must be accurately recorded, dated, and signed. If a correction is needed to a paper record, we recommend that a single line through the incorrect or illegible phrase or passage be made. If you are audited, an outside reviewer must be able to readily see the original passage. Next, the corrected entry should be carefully written next to or above the original entry. It should then be signed and dated by the individual making the correction. The bottom line is simple. An outside third party should never be misled in any way about what was originally recorded or written in a patient’s record, when a corrected entry was made and the identity of the person making a change or supplementing a patient’s dental record. You should also be aware that electronic medical records can typically be audited to determine what changes were made to the records and when. |

| Retain a copy of any information that you submit to the auditor. Make sure that you secure a complete copy of the documentation sent to the payor. It should be “Bates Labeled” and kept separate from your working files. Should an appeal prove necessary, you will need to know the information on which the payor based its denial decision. |

VI. Conclusion:

Dentists enrolled as participating providers in governmental and/or private payor insurance plans are likely to face a variety of audit and enforcement challenges in 2026. Realistically, dental providers should expect audits to continue to be initiated and pursued by the government and by private payor SIUs. The attorneys at Liles Parker have considerable experience representing dentists and dental practices in Medicaid and private payor audits. Click here to schedule an initial complimentary consultation with Liles Parker.

- [1] Palmetto GBA has a published an article titled “Determining Inextricable Linkage for Dental Services” that does a great job of explaining the types of evidence that the contractor will consider when deciding whether a dental service is “inextricably linked” to a covered Medicare medical procedure or service.

- [2] As an example, please see our recent article titled “Delta Dental Audits will Increase in 2026. Is Your Practice Ready.”

- [3] Although Medicare Part A does not cover most dental care treatment services, it may cover certain dental procedures that are necessary for an otherwise covered service to be completed. For instance, a Medicare patient may obtain coverage for certain dental work in connection with jaw surgery. Additionally, several Medicare Advantage plans now cover routine vision and dental procedures.

- [4] Jordan Uditsky is an attorney with Grogan, Hesse & Uditsky, P.C. and represents individuals and entities in the purchase and sale of dental practices.

- [5] See 18 U.S.C. 1347,

- [6] Pursuant to statutory changes enacted by passage of the Affordable Care Act (ACA), 42 U.S.C. § 1320a-7b(g), was modified so that a claim including items or services arising out of conduct that is a violation of the Anti-Kickback Statute, can be pursued as a civil violation of the False Claims Act. This statutory change created an automatic link for civil recovery, even though the conduct would also qualify as criminal conduct for violating the Anti-Kickback Statute.

- [7] See 42 U.S.C. 1320a-7k(d).

- [8] See 42 C.F.R. § 489.41.

- [9] See the Centers for Disease Control and Prevention’s (CDC’s) guidance on injection safety. (March 26, 2024).

- [10] Our chart is based on data from ADA News. (August 6, 2024).

- [11] See Private Equity Stakeholder Project’s report titled “Private Equity Health Care Acquisitions – August 2025.”

- [12] Although Original Medicare (Parts A and B) generally does not cover routine dental services (such as exams, fillings, radiographs, dentures, cleanings, etc.), some Medicare Advantage plans are now offering coverage of both preventative dental services and more comprehensive dental procedures. The extent of coverage varies from Advantage plan to Advantage plan.

- [13] Last year, eleven State Attorneys General sent a joint set of comments in response to the “Request for Information on Consolidation in Healthcare Markets” jointly issued by the Department of Justice (DOJ), the Department of Health and Human Services (HHS), and the Federal Trade Commission (FTC). Their comments detailed how private equity's healthcare acquisitions harm patients, workers, and taxpayers, citing increased costs, lower quality of care, and reduced access by patients.

- [14] As discussed in a recent article by Stateline, seven states (California, Indiana, Massachusetts, Maine, New Mexico, Oregon, and Washington) have enacted laws requiring more oversight over private equity acquisitions in health care.

- [15] For additional information on “Incident To” billing, please see our articles titled: (1) “Incident To Billing Practices are Under Law Enforcement’s Microscope. Are Your Incident To Billing Practices Compliant?” (2022), and (2) “The Dangers of Billing Payors for the Services of a Non-Credentialed Dentist / Non-Participating Dentist.” (2019).

- [16] See 22 Tex. Admin. Code Sec. 108.8 – Records of the Dentist

- [17] Section 6401 of the Affordable Care Act (ACA) provides that a “provider of medical or other items or services or supplier within a particular industry sector or category” shall establish a compliance program as a condition of enrollment in Medicare, Medicaid, or the Children’s Health Insurance Program (CHIP).